Under TDS (Tax Deducted at Source) regulations, TDS must be deducted when the amount is paid or credited to the payee's account, whichever comes first. When an amount is credited to a provisional account, it is considered as credited to the payee's account, and TDS must be deducted accordingly. Therefore, TDS should be deducted even on provisions made in the books of accounts to which TDS provisions are applicable.

A provisional entry for expenses is used to record a calculated or budgeted expense in the accounting system before it is incurred or paid. This entry is based on an estimate when the exact amount or timing of the expense is unsure.

A provisional entry should be posted first, followed by the actual entry. Once the actual entry is posted, the provisional entry should be reversed. As per the requirement, TDS should be calculated on the provisional entry. When the actual entry is posted, the system should not calculate TDS again, since it was already deducted on the provisional entry.

Process

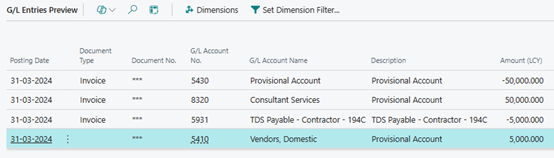

In this scenario, we are assuming the creation and posting of a provisional entry for an expense of 50,000 in March 2024, with the bill to be received after April 2024. TDS at 10% should be calculated on the expense amount.

Provisional Entries via GJ

In Business central user will pass GJ for provisional entry with below details: -

Document type – Invoice

Party type – Vendor

Party code – Vendor ID (ex. V00100)

Account type – G/L Accounts

Account - Provisional Account (ex. 5430)

Amount – (50,000) (in Negative)

Ba. Account type - Expense Account

Location State code – MH (Required location)

Provisional Entry – Mark check box

TDS Section code – 194C (Required TDS section)

Gen. Posting type – Purchase

Gen Bus Posting Group – Required

Gen Prod. Posting group – Required

Location code – Required

T.A.N No – Required

Note: - Since the above entry is being posted at year-end in March, we will process the TDS payment to the government for the last quarter of the year. The process outlined can also be used for monthly provisional expenses. In such cases, the TDS payment entry will not be part of these transactions.

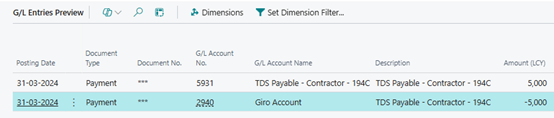

TDS Payment entry via Payment Journals

In Business central user will pass Payment Journals for TDS payment with below details: -

Document type – Payment

Account type – G/L Accounts

Account Number – 5931(TDS GL account for section 194C)

Payment Method Code – Required

Location code – Required

T.A.N. No – Required

T.C.A.N No – Required

Bal. Account type – Required (Bank)

Bal. Account Number – Required

Click on Pay TDS à TDS

Click on Pay

System will update the Amount

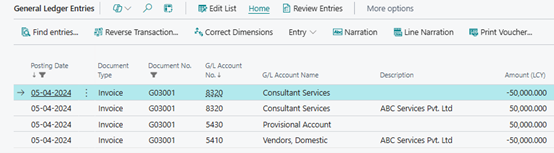

Actual Invoice via Purchase Journal

In Business central user will pass Actual invoice via Purchase Journal with below details: -

Document type – Invoice

Account Type – Vendor

Account No – Required (Select the same vendor that was chosen when creating the provisional entry)

TDS section – Blank

Balance Account – Actual Expense Account (in this case 8320)

Amount – (-50,000) (actual amount used in provisional entry)

Location code – Same as Provisional Entry

External Document Number – Required

Click on action à Apply Provisional Entry à Select related entry à Click on Apply